How to Tax Our Way Back to Justice

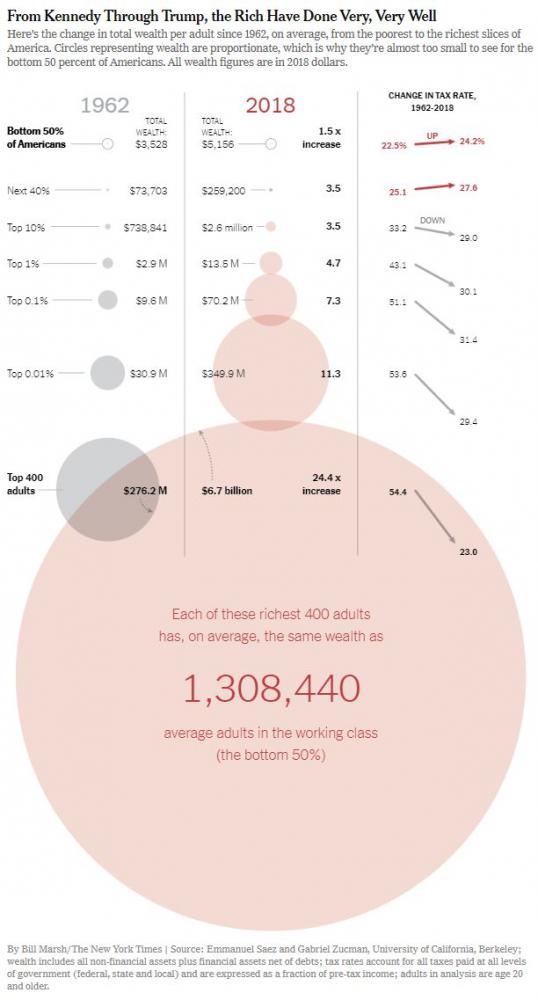

America’s soaring inequality has a new engine: its regressive tax system. Over the past half century, even as their wealth rose to previously unseen heights, the richest Americans watched their tax rates collapse. For the working classes over the same period, as wages stagnated, work conditions deteriorated and debts ballooned, tax rates increased.

Stop to think this over for a minute: For the first time in the past hundred years, the working class — the 50 percent of Americans with the lowest incomes — today pays higher tax rates than billionaires.

The full extent of this situation is not visible in official statistics, which is perhaps why it has not received more attention. Government agencies like the Congressional Budget Office publish information about the distribution of federal taxes, but they disregard state and local taxes, which account for a third of all taxes paid by Americans and are in general highly regressive. The official statistics keepers do not provide specific information on the ultra-wealthy, who although few in number earn a large fraction of national income and therefore account for a large share of potential tax revenue. And until now there were no estimates of the total tax burden that factored in the effect of President Trump’s tax reform enacted at the end of 2017, which was particularly generous for the ultra-wealthy.

To fill this gap, we have estimated how much each social group, from the poorest to billionaires, paid in taxes for the year 2018. Our starting point is the total amount of tax revenue collected in the United States, 28 percent of national income. We allocate this total across the population, divided into 15 income groups: the bottom 10 percent (the 24 million adults with the lowest pretax income), the next 10 percent and so on, with finer-grained groups within the top 10 percent, up to the 400 wealthiest Americans.

Our data series include all taxes paid to the federal, state and local governments: the federal income tax, of course, but also state income taxes, myriad sales and excise taxes, the corporate income tax, business and residential property taxes and payroll taxes. In the end, all taxes are paid by people. The corporate tax, for example, is paid by shareholders, because it reduces the amount of profit they can receive in dividends or reinvest in their companies.

You will often hear that we have a progressive tax system in the United States — you owe more, as a fraction of your income, as you earn more. When he was a presidential candidate in 2012, Senator Mitt Romney famously lambasted the 47 percent of “takers” who, according to him, do not contribute to the public coffers. In reality, the bottom half of the income distribution may not pay much in income taxes, but it pays a lot in sales and payroll taxes. Taking into account all taxes paid, each group contributes between 25 percent and 30 percent of its income to the community’s needs. The only exception is the billionaires, who pay a tax rate of 23 percent, less than every other group.

The tax system in the United States has become a giant flat tax — except at the top, where it’s regressive. The notion that America, even if it may not collect as much in taxes as European countries, at least does so in a progressive way, is a myth. As a group, and although their individual situations are not all the same, the Trumps, the Bezoses and the Buffetts of this world pay lower tax rates than teachers and secretaries do.

This is the tax system of a plutocracy. With tax rates of barely 23 percent at the top of the pyramid, wealth will keep accumulating with hardly any barrier. So, too, will the power of the wealthy, including their ability to shape policymaking and government for their own benefit.

The good news is that we can fix tax injustice, right now. There is nothing inherent in modern technology or globalization that destroys our ability to institute a highly progressive tax system. The choice is ours. We can countenance a sprawling industry that helps the affluent dodge taxation, or we can choose to regulate it. We can let multinationals pick the country where they declare their profits, or we can pick for them. We can tolerate financial opacity and the countless possibilities for tax evasion that come with it, or we can choose to measure, record and tax wealth.

If we believe most commentators, tax avoidance is a law of nature. Because politics is messy and democracy imperfect, this argument goes, the tax code is always full of “loopholes” that the rich will exploit. Tax justice has never prevailed, and it will never prevail.

For example, in response to Elizabeth Warren’s wealth tax proposal — which we helped develop — pundits have argued that the tax would raise much less revenue than expected. In a similar vein, world leaders have become convinced that taxing multinational companies is now close to impossible, because of international tax competition. During his presidency, Barack Obama argued in favor of reducing the federal corporate tax rate from 35 percent to 28 percent, with a lower rate of 25 percent for manufacturers. In 2017, under President Trump, the United States cut its corporate tax rate to 21 percent. In France, President Emmanuel Macron is in motion to reduce the corporate tax in 2022 to 25 percent from 33 percent. Britain is ahead of the curve: It started slashing its rate under Prime Minister Gordon Brown in 2008 and is aiming for 17 percent by 2020. On that issue, the Browns, Macrons and Trumps of the world agree: The winners of global markets are mobile; we can’t tax them too much.

But they are mistaken. Tax avoidance, international tax competition and the race to the bottom that rage today are not laws of nature. They are policy choices, decisions we’ve collectively made — perhaps not consciously or explicitly, certainly not choices that were debated transparently and democratically — but choices nonetheless. And other, better choices are possible.

Take big corporations. Some countries may have an interest in applying low tax rates, but that’s not an obstacle to making multinationals (and their shareholders) pay a lot. How? By collecting the taxes that tax havens choose not to levy. For example, imagine that the corporate tax rate in the United States was increased to 35 percent and that Apple found a way to book billions in profits in Ireland, taxed at 1 percent. The United States could simply decide to collect the missing 34 percent. Apple, like most Fortune 500 companies, does in fact have a big tax deficit: It pays much less in taxes globally than what it would pay if its profits were taxed at 35 percent in each country where it operates. For companies headquartered in the United States, the Internal Revenue Service should collect 100 percent of this tax deficit immediately, taking up the role of tax collector of last resort. The permission of tax havens is not required. All it would take is adding a paragraph in the United States tax code.

The same logic can be applied to companies headquartered abroad that sell products in America. The only difference is that the United States would collect not all but only a fraction of their tax deficit. For example, if the Swiss food giant Nestlé has a tax deficit of $1 billion and makes 20 percent of its global sales in the United States, the I.R.S. could collect 20 percent of its tax deficit, in addition to any tax owed in the United States. The information necessary to collect this remedial tax already exists: Thanks to recent advances in international cooperation, the I.R.S. knows where Nestlé books its profits, how much tax it pays in each country and where it makes its sales.

Collecting part of the tax deficit of foreign companies would not violate any international treaty. This mechanism can be applied tomorrow by any country, unilaterally. It would put an end to international tax competition, because there would be no point any more for businesses to move production or paper profits to low-tax places. Although companies might choose to stop selling products in certain nations to avoid paying taxes, this would be unlikely to be a risk in the United States. No company can afford to snub the large American market.

These examples are powerful because they show, contrary to received wisdom, that the taxation of capital and globalization are perfectly compatible. The notion that external or technical constraints make tax justice idle fantasy does not withstand scrutiny. When it comes to the future of taxation, there is an infinity of possible futures ahead of us.

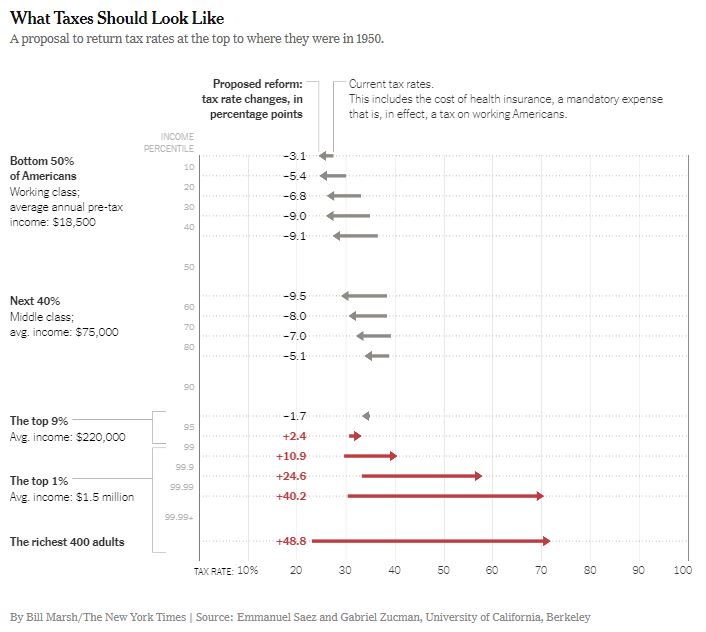

Are these ideas for greater economic justice realistic politically? It is easy to lose hope — money in politics and self-serving ideologies are powerful foes. But although these problems are real, we should not despair. Before injustice triumphed, the United States was a beacon of tax justice. It was the democracy with the most steeply progressive system of taxation on the planet. In the 1930s, American policymakers invented — and then for almost half a century applied — top marginal income tax rates of close to 90 percent on the highest earners. Corporate profits were taxed at 50 percent, large estates at close to 80 percent.

The history of taxation is full of U-turns. Instead of elevating some supposedly invincible and natural constraints — that are often invincible and natural only in terms of their own models — economists should act more like plumbers, making the tax machinery work, fixing leaks. With good plumbing — and if the growing political will to address the rise of inequality takes hold — there is a bright future for tax justice.

More by and About Saez and Zucman

The Rich Really Do Pay Lower Taxes Than You

How Corporations and the Wealthy Avoid Taxes (and How to Stop Them)

Emmanuel Saez and Gabriel Zucman (@gabriel_zucman) are economists at the University of California, Berkeley, and the authors of “The Triumph of Injustice: How the Rich Dodge Taxes and How to Make Them Pay,” from which this essay is adapted.

The Times is committed to publishing a diversity of letters to the editor. We’d like to hear what you think about this or any of our articles. Here are some tips. And here’s our email: letters@nytimes.com.

Follow The New York Times Opinion section on Facebook, Twitter (@NYTopinion) and Instagram.