Common Tax ‘Reform’ Questions, Answered

Should tax cuts be today’s policy priority?

No. Tax cuts provide no durable solution to any genuine economic problem for America’s working families, but do make some genuine problems even worse.

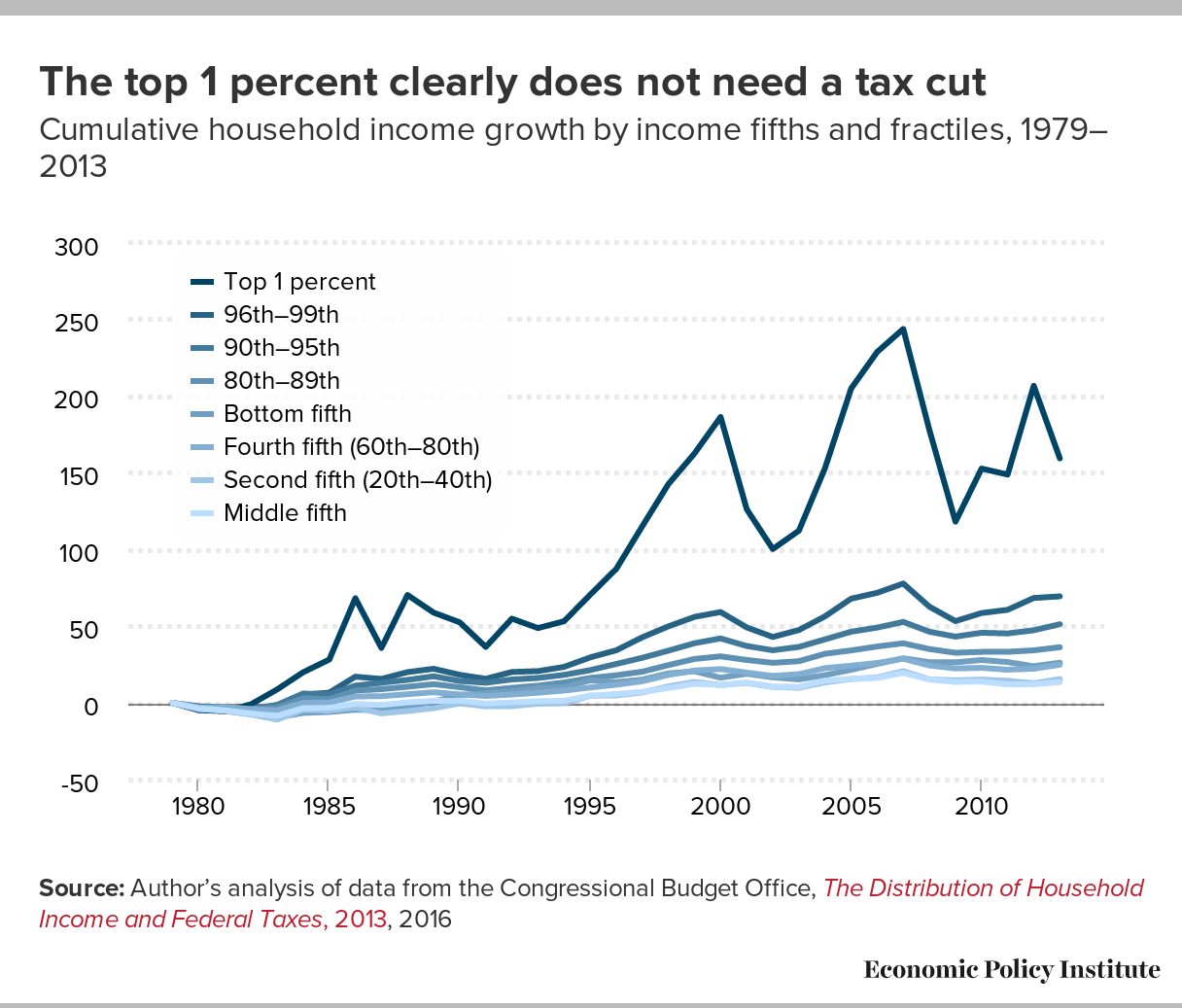

Most Republican plans, including the new “Big 6” framework released at the end of September, prioritize cutting top income tax rates and rates paid by corporations.1 These rate cuts would lead to huge benefits for the already-rich, but provide just crumbs to low- and middle-income families. For example, the Tax Policy Center estimates that about 50 percent of all benefits from the Big 6 proposal would accrue to the top 1 percent.2 This top 1 percent has seen income growth of 160 percent since 1979, compared with growth of 13.6 percent for the middle 20 percent of families.3 In short, the top 1 percent doesn’t need a tax cut, yet this is exactly the group that Republican tax plans aim to help.

{kind=link}

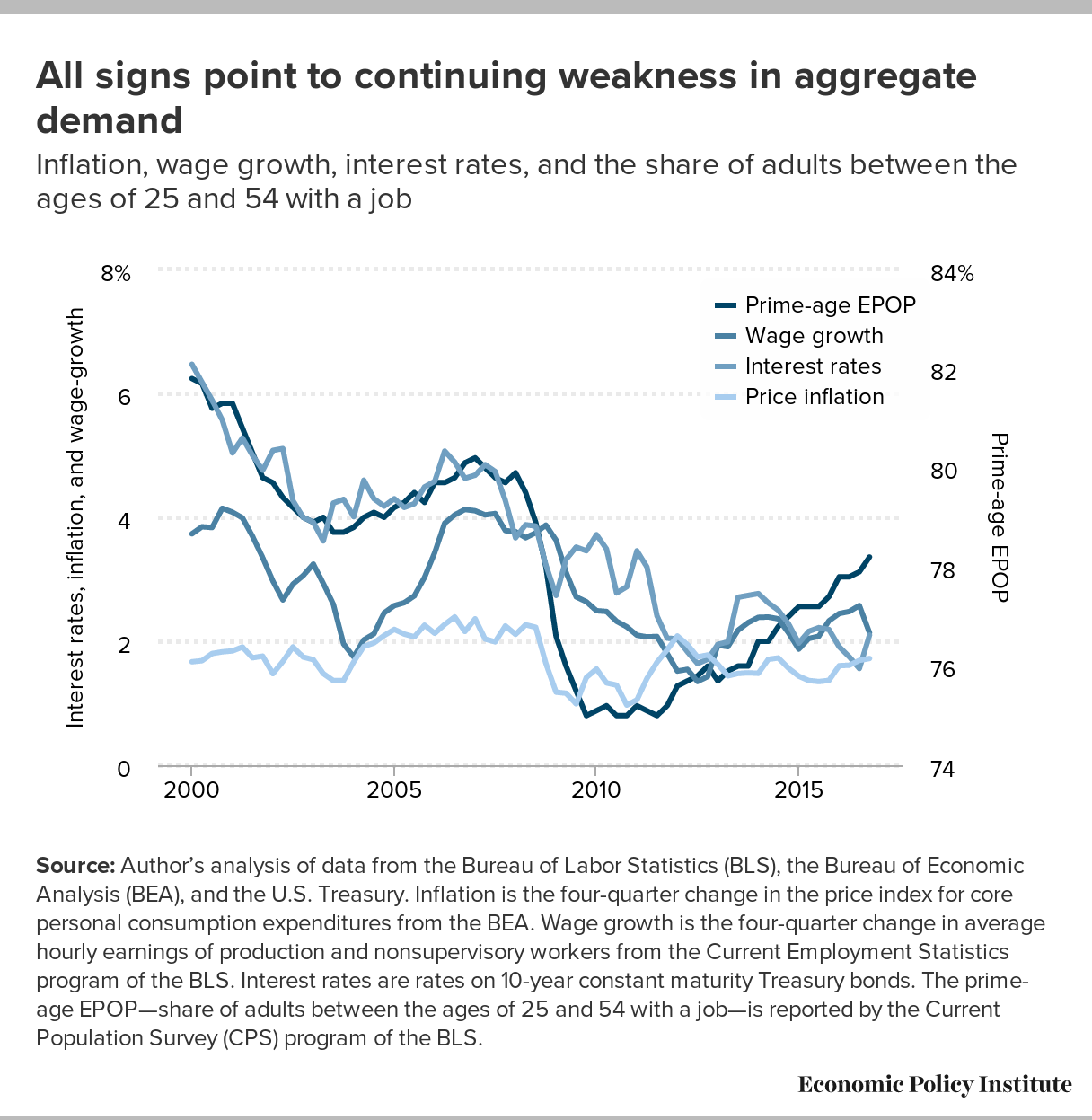

Importantly, the problem for vast majority of American households has not been what taxes have taken out of their paychecks in recent decades, but what employers have not been putting into these paychecks.

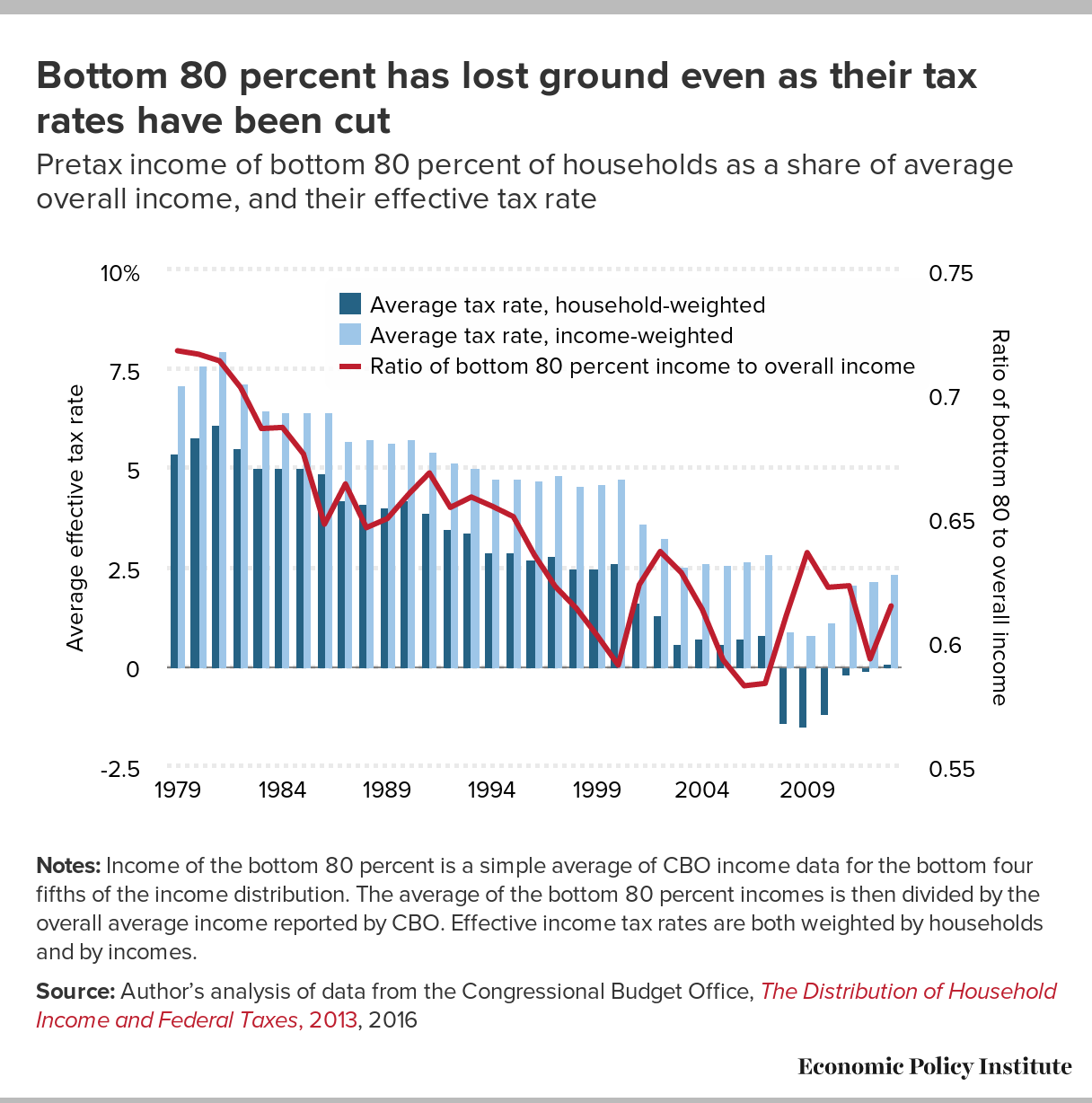

Taxes are not the reason why low- and middle-income households have seen weak income growth in recent decades. Effective federal tax rates for the bottom 80 percent of households have fallen dramatically since 1979.4 Despite these lower taxes, income growth has been anemic because of a range of intentional policy decisions that have shifted economic power away from low- and moderate-wage workers toward capital-owners and corporate managers.5 Tax cuts for the rich would just further direct resources to the top of the income distribution, and would also provide even greater incentive for capital-owners and corporate managers to rig the economic rules to send more income their way.6 Solving the problem of degraded economic leverage leading to near-stagnant pay for the broad middle class should be the economic priority of Congress.7

{kind=link}

Finally, tax cuts will reduce federal revenues in coming years at a time when we will need greater revenues to honor existing federal commitments to provide health care for Americans.

The federal government is the single largest payer of health care costs in the economy, and these health care costs have grown faster than overall economic growth for decades. The federal health programs—Medicare, Medicaid, and the Affordable Care Act—are efficient and do a better job at containing costs than private insurance.8 Cutting these programs would be inefficient and, worse, just shift health care costs onto American household budgets. In short, Medicare, Medicaid, and the ACA are valuable investments that we should finance, not starve of revenue.

{kind=link}

Would cutting corporate tax rates boost American jobs?

No. Corporate tax cuts are about the worst fiscal tool we have for boosting job growth.

In an economy constrained by too-slow spending (or a lack of aggregate demand, in economists’ jargon), tax cuts can in theory boost demand by raising (post-tax) incomes and inducing households to spend more. But the bulk of corporate tax cuts would benefit the richest Americans, and these households are far less likely to spend an additional dollar for every dollar in tax cuts than low- or middle-income households. To put it simply, spending of rich households is not constrained by too-low incomes, so giving them more income does little to induce more spending.

If Congress wants to spur demand and create jobs with fiscal policy changes, it should either target tax cuts at low- and middle-income families, or boost spending directly. This recommendation is clearly borne out by all serious economic evidence: in a ranking of fiscal policy changes based on bang for the buck—how many jobs they create—corporate rate cuts are near the bottom of the list.9

Would cutting corporate tax rates boost American investment or wages?

No. Companies are not investing in the things that could boost wages by making workers more productive (plants and equipment, technology, research) because of insufficient demand, not because they don’t have the profits to invest or because they face high interest rates.

If the economy’s growth is not constrained by too-slow spending, then there is a theoretical case that corporate rate cuts could boost growth by encouraging investments that increase the economy’s productive capacity (“supply side” effects). However, today’s real-world data indicate strongly that this theoretical case will fail.

The argument that corporate rate cuts would boost investment in plants and equipment depends on a long chain of influences. Here is how it would work theoretically. First, by boosting the post-tax return to owning capital like stocks and bonds, the rate cuts induce households to save more. Next, this increased supply of savings drives down economy-wide interest rates. This fall in interest rates then induces firms to borrow more to invest in plants and equipment. The new plant and equipment investments give workers better tools to do their jobs, boosting productivity and thus (as many assume) mechanically boosting wages.

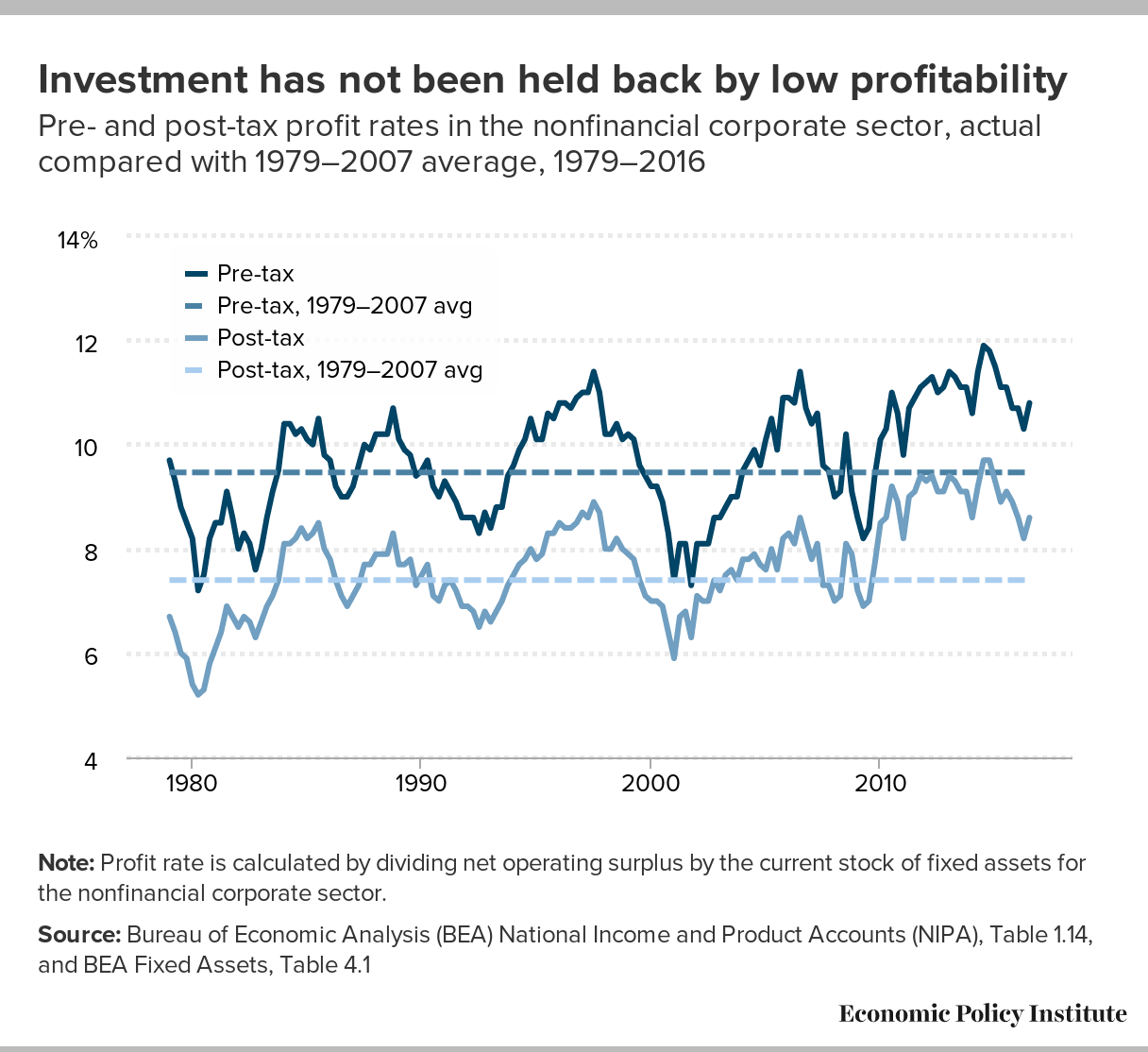

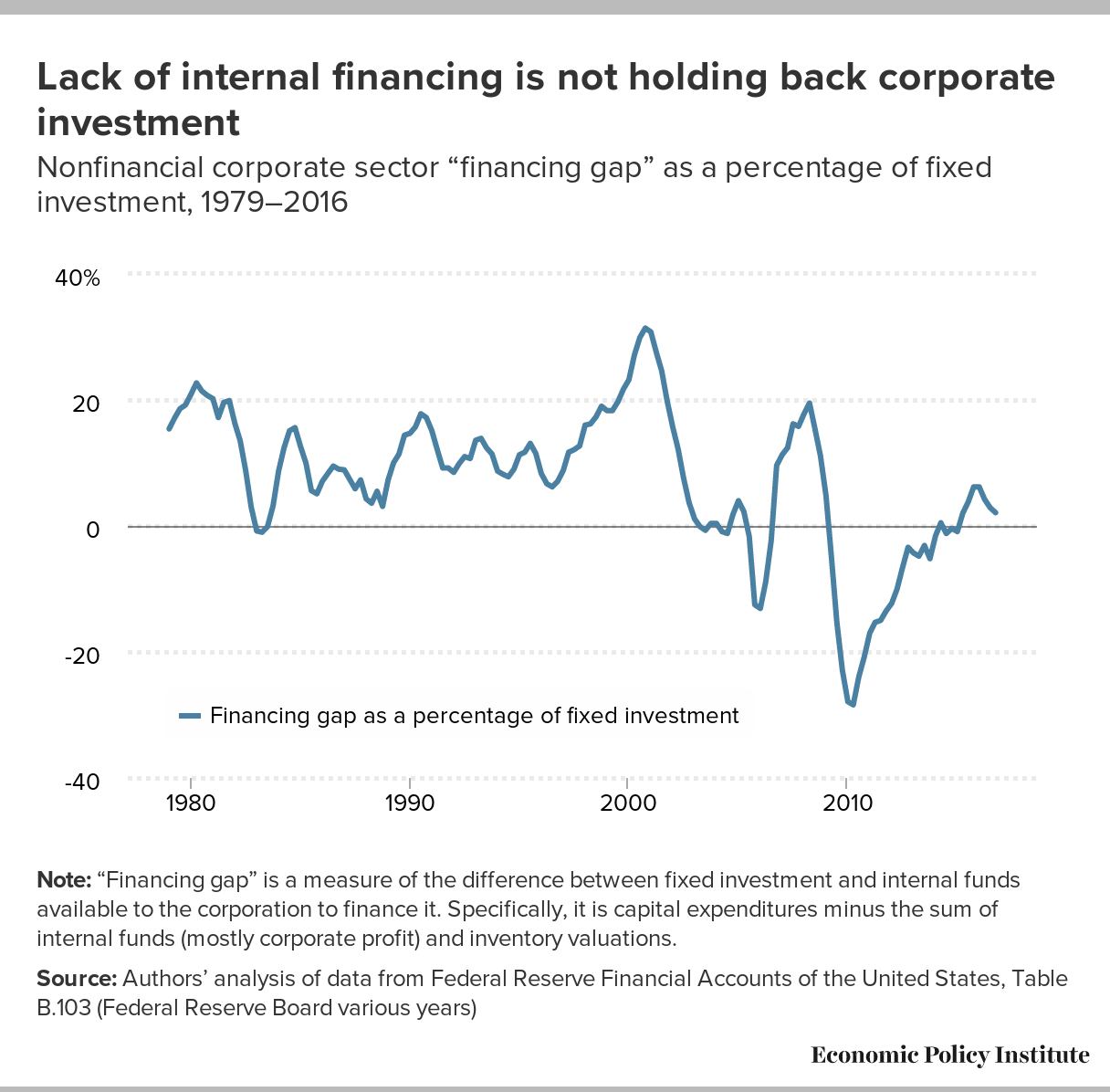

But nearly every link in this chain fails when faced with today’s real-world data. For one thing, post-tax corporate profit rates remain historically elevated, down just a bit from the historical peaks they hit in recent years.10 Yet these higher rates have not been associated with rapid investment in plants and equipment in recent years. For another thing, we don’t currently have a situation in which deficient savings is leading to high interest rates and thus depressing investment. Corporate savings are high11 and interest rates remain extremely low12 relative to historical data. The combination of low interest rates and low investment with high profit rates signals extraordinarily strongly that the constraint on investment is sluggish demand, not insufficient savings. This means that policy changes that reduce spending (consumption) to boost savings are actually likely to slow growth, not boost it.

{kind=link}

{kind=link}

And there are even more fundamental problems with the logic of the “tax cuts will boost savings” link in the chain. While corporate rate cuts can boost household savings, they unambiguously reduce public savings by increasing the federal budget deficit. This makes their effect on total national savings (the relevant measure for influencing interest rates) a wash at best. So corporate rate cuts alone will not boost savings unless paired with spending cuts or other tax increases.

Finally, even if insufficient savings were the problem and somehow corporate tax cuts did boost plant and equipment investment and boost productivity, this still doesn’t guarantee that wages for the vast majority of American workers would rise. Wages for the vast majority of U.S. workers stopped rising in tandem with productivity decades ago.13 Workers are more valuable but companies aren’t paying them more. The disconnect between productivity growth and wage growth is the result of a set of intentional policy decisions that have eroded the bargaining power of workers.14 Cutting corporate tax rates is not the solution that will reverse this trend.

Is it a problem that tax cuts (including corporate rate cuts) add to the federal budget deficit?

Yes and no. The boost to the deficit is a problem for proponents of the tax plan because it invalidates their claims about the benefits of tax cuts. While real-world evidence shows that deficits are not a pressing economic problem, deficits often create (largely misguided) political pressure to cut spending on valuable programs critical to America’s working families, such as Social Security, Medicare, Medicaid, and the Affordable Care Act.

Proponents of tax cuts for rich households and corporations often claim that they would boost investment, productivity, and wages. But this would only be true if the tax cuts (particularly the cuts on capital incomes) boost savings, drive down interest rates, and encourage corporations to invest in plants and equipment. But even if the tax cuts were to spur an increase in household savings, they would also unambiguously reduce public savings by increasing the federal budget deficit. So tax cuts by themselves cannot work the way their proponents claim—the cuts need to be offset with either increases in other taxes or spending cuts to neutralize their effect on public savings. This fact is why honest efforts to “dynamically score” plans like the recent “Big 6 proposal” backed by the Trump administration routinely find the plans will actually reduce growth and job creation.15

Given today’s real-world data, it is clear that federal budget deficits are not a pressing economic problem now and are not likely to be a problem in the short- or medium-term.16 The U.S. economy’s fiscal position is fundamentally solid. Long-term interest rates and inflation remain low. But if tax cuts for the rich feed the “deficit hysteria” that infects so much of Beltway policymaking, this would pose a problem. In today’s economy of slack demand, anything that convinces policymakers to cut spending on valuable programs will not only hurt the families who rely on those programs but drag on growth and prolong the years-long failure to return the economy to genuine full employment..

{kind=link}

Do U.S. corporations pay significantly more in income taxes than companies in our peer countries?

No. American corporations are clearly not heavily taxed relative to international norms.

While the statutory U.S. corporate tax rate of 35 percent is on the high end internationally, corporations don’t actually pay anywhere near that rate on average. Using loopholes to avoid paying their full tax bills, corporations pay an effective tax rate of between 12.5 percent and 21.2 percent.17 One of the key loopholes is deferral—which allows U.S. firms to pay zero taxes on profits booked overseas (often through clever accounting practices) unless and until those profits are “repatriated” (returned) to owners in the United States.

Measured as a share of total GDP, U.S. corporations pay significantly less than their international peers. In 2015, the revenue raised through U.S. corporate taxes equaled 2.2 percent of GDP. On average, other member countries of the Organization for Economic Cooperation and Development (OECD) raised 2.9 percent of GDP through corporate taxes.18

Does the U.S. corporate tax code harm American workers by making U.S. firms less “competitive”?

No. The “competitiveness” claim is just hand-waving to disguise the fact that corporate tax cuts do not boost wages or jobs for U.S. workers, and that the effective rates U.S. corporations pay are not out of line with our international peers.

While cutting U.S. corporate rates would render U.S. corporations more profitable, these cuts would do nothing to boost jobs or wages for American workers—through increased “competitiveness” or any other channel. U.S. corporate profits are historically high and yet U.S. corporations aren’t investing a lot more in plants, research, and new technology.19

Key to understanding why this competitiveness argument is a pure dodge is the fact that the United States taxes firms on a worldwide basis, meaning that profits are taxed at the same rate whether they’re booked domestically or internationally. So, cutting corporate tax rates would just reduce the rates U.S. firms pay on profits here and abroad, which does nothing to encourage corporations to set up plants here in the United States. Not only that, the deferral loophole allows U.S. firms to avoid paying taxes on profits booked overseas until profits repatriate to the firms’ owners in the United States. Because the deferral loophole encourages corporations to keep accounting profits overseas, one obvious way to improve the “competitiveness” of the U.S. corporate tax code is to reduce the share of corporate profits appearing overseas by ending deferral and requiring that corporations pay their taxes when the income is earned—just like American families do.

Finally, some purveyors of the “competitiveness” argument imply that U.S. corporations might do better in claiming global market share against foreign corporations if our corporate rates were cut. But this would only be true if corporate rate cuts somehow translated into lower prices for the output of American firms, and no serious economist thinks this would happen. All in all, claims that U.S. corporate rates should be cut in the name of boosting American competitiveness are economic snake oil.

Does the U.S. corporate tax code force businesses to move their headquarters overseas? Even if it did, is this necessarily bad for American workers?

No. Tax loopholes allow some firms to use financial engineering to make profits look like they were earned overseas, but these firms are not generally moving actual factories and jobs overseas. The solution to this problem of international tax avoidance isn’t to give up on collecting taxes; it’s to close the loopholes.

Current U.S. tax laws are already outrageously generous to tax-dodging multinational corporations. Under the deferral loophole, firms avoid paying taxes indefinitely by using accounting tricks to make profits appear to have been booked in subsidiaries overseas.

Deferrals are encouraged by the prospect of ad hoc “tax holidays,” when the U.S. government gives companies that bring profits back to the U.S. in a given year a deep discount on their tax bill. For example, in 2004, legislation passed by Congress allowed companies to pay just 5.25 percent on repatriated profits, dramatically lower than the 35 percent statutory tax rate. But there hasn’t been a tax holiday on deferred overseas profits since 2004, and this has made some companies with huge offshore profits worried that they might actually have to pay the full taxes they owe on all the profits they’ve stashed overseas.

Instead of waiting and risking a future Congress that changes tax law to actually collect the full amount of taxes owed on overseas profits, some of these companies are engaging in the do-it-yourself permanent tax break known as an “inversion.” In an inversion a U.S. multinational is “bought” by a foreign company that is small enough that the original corporation can still retain managerial control over the new company. The new, now ostensibly foreign company then uses accounting gimmicks to ensure that its U.S. tax bill is zero.

But these firms generally do not move productive plants and equipment and jobs overseas; instead, they just move paper profits. To put it simply, U.S. manufacturing jobs are not moving to tax havens such as Ireland or the Cayman Islands, accounting profits are moving there and avoiding taxes, and that’s the key problem we should try to solve with corporate tax reform.

Inversion is clearly nothing but a strategy to dodge taxes. In 2016, the Obama administration clamped down on one loophole that multinationals use to claim tax savings once they’ve inverted. Lo and behold, a planned inversion by Pfizer was immediately halted.20 There’s no point in pretending you’re being bought if you’re just going to have to pay your taxes anyway.

Do small business owners need a tax cut to level the playing field with larger corporations?

No. Arguments over business tax reform often misleadingly imply that there is a “small business tax rate” that could be cut to help out small business owners. There is no small business tax code in the United States.

Small businesses in the United States are not taxed at the business level, while corporations are. Instead, owners of small businesses pay taxes on the profits they make when they pay individual income taxes, as do owners of corporations (shareholders) when these corporations return business profits to them in the form of dividends or capital gains. This means that owners of small businesses are not disadvantaged relative to owners of corporations by the American tax code.

Further, capping the rate applied to “pass-through” income (income returned to owners of businesses that are not taxable corporations) declared on individual tax returns at 25 percent—as the “Big 6 proposal” does—would only help those business owners who net more than $250,000 per year in business income after expenses. Such business owners constitute well under 3 percent of tax filers. In short, what is generally advertised as a cut to “small businesses” is just one more cut to the richest households, particularly those who hire good accountants to make their individual income appear to be pass-through income.

To be clear, there are plenty of nontax policies that should be undertaken to help small businesses, particularly policies that would allow them to compete more effectively with corporations. Robust competition policy that restrains the power of monopolies would be a huge boon to small businesses. And small businesses would benefit greatly from macroeconomic policies (such as federal spending and continued low interest rates) that finally restored the economy to genuine full employment by boosting aggregate demand.

In summary, small businesses don’t pay taxes at the business level, corporate rate cuts will not help them, and cuts to top individual tax rates or to rates on capital income earned by individuals is much more likely to benefit the owners of corporations than the owners of small businesses.

Do U.S. corporations need tax cuts to resolve economic “uncertainty” that is supposedly holding back U.S. growth?

Uncertainty is not what is holding back economic growth—a continuing shortfall of aggregate demand (spending by households, businesses, and governments) is.

Blaming slow growth on uncertainty is a smokescreen. If members of Congress truly believed that “uncertainty” were stymieing growth, they could pass a resolution assuring corporations that absolutely no new tax cuts would be forthcoming. “Certainty” then is not what corporations are really looking for. What they’re really looking for are tax breaks.